Signals

A company intelligence agent built on Claude and CrewAI

Real World Application

Built for the research work that happens before a QBR, renewal conversation, enterprise prospect call, vendor evaluation, or job interview. Signals replaces the tab-switching, time-intensive copy-pasting workflow of stitching together multiple individual Google searches. The structured output — Fundamentals, Product, Customers, and Market — provides key insights into a company's current scale, core value proposition and key differentiators, market position and competitive landscape, and growth and expansion trajectory. The onboard chat turns a static report into a dynamic research session, letting you go deeper into the specific insights that matter for the conversation you're about to have.

Signals is configured specifically for B2B SaaS company research, but the prompt architecture and report structure can be reconfigured for any industry or research context.

Signals automatically exports each research report so it can be reviewed offline or imported into a new session at a later date. Every agent chat can also be copied or downloaded. The two reports below show the structured research output and how the agent handles information it can't fully verify or must infer. The two chat sessions give a feel for how the agent reasons.

ChurnZero vs. Totango Chat

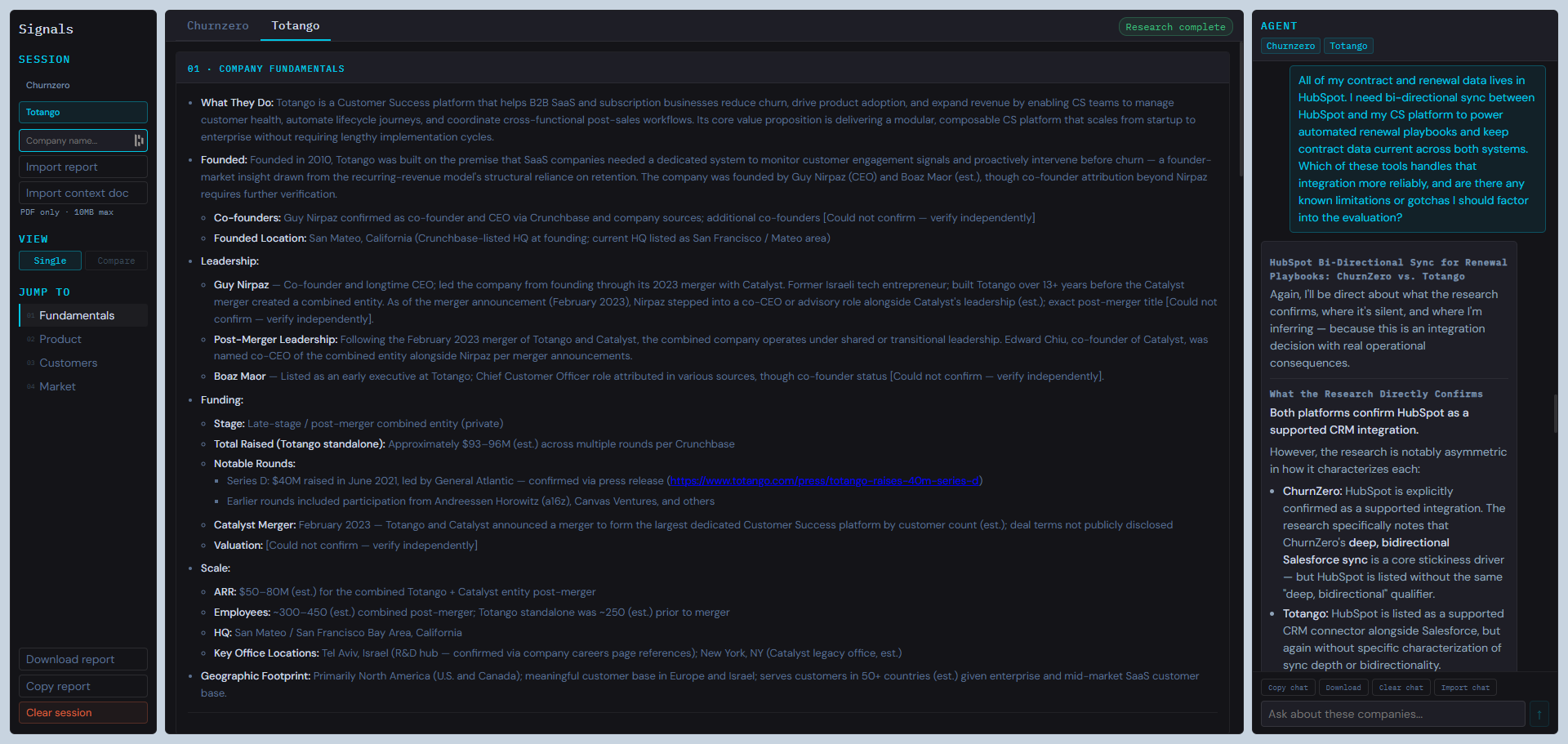

**You:** Summarize the key similarities and differences between these companies. **Agent:** # ChurnZero vs. Totango: Comparative Analysis --- ## CORE SIMILARITIES **Same category, same buyer, same daily user.** Both are purpose-built Customer Success platforms targeting B2B SaaS companies with subscription revenue. The buyer is a VP of CS or CCO; the daily user is a CSM. Both compete on the same core value proposition: reduce churn, improve NRR, and scale CS team efficiency through health scoring and playbook automation. **Functionally overlapping product sets.** Both offer: - Configurable customer health scoring (usage data, CRM inputs, support signals, NPS) - Automated playbooks/plays triggered by health changes - CSM workspace/cockpit for account management - Deep Salesforce and HubSpot CRM integrations - Similar adjacent integrations (Zendesk, Stripe, Segment, Slack) **Same competitive enemy at the top.** Both position against Gainsight as the bloated, expensive, slow-to-implement enterprise incumbent — and win deals by offering faster time-to-value and better mid-market fit. **Similar switching cost profile.** Both become sticky through health score history, playbook configurations, and deep CRM integration — all of which are painful to migrate off. --- ## KEY DIFFERENCES ### Scale & Maturity | Dimension | ChurnZero | Totango | |---|---|---| | **Founded** | 2015 | 2010 | | **Total Funding** | ~$35M | ~$93–96M | | **Est. ARR** | $30–60M | $50–80M (post-merger) | | **Employees** | ~300–350 | ~300–450 (post-merger) | Totango is the older, better-funded company with a larger installed base — but ChurnZero has closed the gap rapidly from a much smaller capital base, suggesting stronger capital efficiency. --- ### Market Position & ICP **ChurnZero** is a **mid-market specialist** — tightly focused on B2B SaaS companies with 50–500 employees and CS teams of 3–30 CSMs. It owns that lane clearly and doesn't credibly compete at large enterprise. **Totango** plays a **broader field** — mid-market through enterprise, with logos like Zoom, SAP, and NTT that ChurnZero doesn't have. Post-Catalyst merger, it is explicitly trying to compete across startup to enterprise. The trade-off is focus: broader market coverage comes with more complex positioning. --- ### Product Philosophy **ChurnZero** differentiates on **real-time data processing** and **native in-app engagement** (Journeys module). Its in-app messaging capability is built into the core platform — not bolted on — reducing the need for a separate Pendo or Appcues tool. The product philosophy is depth-for-the-mid-market. **Totango** differentiates on **SuccessBLOCs** — pre-built, modular CS program templates (onboarding, adoption, renewal, expansion) that allow rapid deployment without custom configuration. The philosophy is *composability and speed*: start with a module, expand as you grow. --- ### Corporate Situation **ChurnZero** is an **independent, organically growing company** — clear ownership, stable leadership (You Mon Tsang as CEO since founding, Abby Hammer as CCO), and a focused roadmap. No M&A complexity. **Totango** is a **post-merger integration story**. The February 2023 merger with Catalyst created a co-CEO structure (Guy Nirpaz + Edward Chiu) and unresolved product roadmap questions. G2 reviews and community feedback reflect customer anxiety about platform consolidation direction. This is an active risk for Totango accounts and an active opportunity for competitors. --- ### Brand & Community **ChurnZero** has invested meaningfully in CS practitioner community — running the **BIG RYG conference** and the **Customer Success Leadership Network (CSLN)**. This gives it strong organic brand equity with the CS persona. G2 rating: **4.7/5** on 1,000+ reviews. **Totango** has weaker top-of-funnel brand presence. It lacks a comparable community/event asset. General Atlantic's backing gives it institutional credibility but not practitioner loyalty. --- ## BOTTOM LINE ChurnZero and Totango are the two most direct mid-market CSP competitors — closer to each other than either is to Gainsight. **ChurnZero wins on focus, brand, and ease of use.** **Totango wins on scale, enterprise reach, and the SuccessBLOCs deployment speed story.** The Catalyst merger gives Totango more market coverage but introduces execution risk that ChurnZero doesn't carry. For a strategic account manager, the single most exploitable difference right now is Totango's post-merger uncertainty versus ChurnZero's organizational stability. **You:** My team has built a custom health scoring model that pulls platform usage data from Snowflake and scores customer engagement across high-value features. Which of these platforms offers more robust support for ingesting custom health signals from an external data warehouse and what does the integration path actually look like for each? **Agent:** ## Custom Health Signal Ingestion: ChurnZero vs. Totango This is a specific technical question that goes beyond what the research explicitly details, so I'll give you what the research directly supports, flag the gaps honestly, and offer reasoned inference where appropriate. --- ## What the Research Directly Confirms **Neither platform's Snowflake integration depth is explicitly documented in the research.** Both platforms confirm: - **REST API** available for custom data ingestion - **Segment and Mixpanel** connectors (both) - **Totango specifically lists Snowflake and Redshift** as data ingestion sources in its ecosystem documentation - **ChurnZero** lists Segment and Mixpanel but **Snowflake is not explicitly confirmed** in the research This is a meaningful difference worth flagging immediately. --- ## Reasoned Assessment by Platform ### Totango — More Likely the Stronger Path (Based on Available Evidence) **What the research supports:** - Snowflake is explicitly listed as a supported data source in Totango's integrations ecosystem - The **SuccessBLOCs architecture** is described as "composable" — designed to ingest external signals and map them to lifecycle stages without requiring full platform reconfiguration - Totango's funding level (~$93-96M vs. ChurnZero's ~$35M) and older vintage (2010 vs. 2015) suggest a more mature data infrastructure layer built to handle enterprise-grade data pipelines **Likely integration path:** 1. **Snowflake → Totango via native connector** — Totango's listed Snowflake support suggests a direct data pipeline, likely using scheduled syncs or reverse ETL patterns to push warehouse-computed scores into Totango as custom attributes or health signal inputs 2. **Map external scores to health score framework** — Totango's configurable health scoring would allow your pre-computed engagement scores to be ingested as weighted inputs alongside native signals (usage, support, NPS) 3. **Trigger SuccessBLOCs from ingested signals** — Once your Snowflake-derived scores land as customer attributes, they can be used to trigger automated playbooks and segment customers **Key unknown:** Whether the Snowflake connector is native/no-code or requires a middleware layer (e.g., Fivetran, dbt, reverse ETL tool like Census or Hightouch). This requires direct verification with Totango's solutions engineering team. --- ### ChurnZero — Viable But Less Certain **What the research supports:** - REST API is confirmed — meaning your Snowflake scores *can* be pushed to ChurnZero programmatically - Segment connector is confirmed — if your Snowflake data flows through Segment, there is a supported path - **Snowflake native connector is not confirmed** in the research — this is a gap that requires direct verification **Likely integration path (inferred):** 1. **Option A — REST API push:** Your data engineering team writes a pipeline that queries Snowflake on a scheduled basis and POSTs custom attribute values (your engagement scores) to ChurnZero via API. This works but requires ongoing engineering maintenance. 2. **Option B — Reverse ETL middleware:** Use a tool like Census, Hightouch, or Polytomic to sync Snowflake-computed scores to ChurnZero as custom fields. This is a common pattern for companies with warehouse-centric data stacks and avoids custom engineering. 3. **Option C — Via Segment:** If your Snowflake scores are already surfaced through Segment, ChurnZero's confirmed Segment connector provides a supported path without API work. **Key concern:** ChurnZero's real-time processing differentiator is most relevant for *native* usage event ingestion. For *externally computed* scores from a warehouse, the real-time advantage may not apply — warehouse sync cadences (hourly, daily) could limit the responsiveness of your health scoring triggers regardless of ChurnZero's internal processing speed. --- ## The Question That Should Drive Your Decision Your use case — **pre-computed scores from an external model** — is architecturally different from a platform consuming raw usage events and computing health internally. You've already done the scoring logic. You need a platform that: 1. **Accepts custom numeric attributes cleanly** (not just binary flags) 2. **Weights external scores appropriately** within the overall health framework 3. **Triggers playbooks from those external score values** with sufficient granularity 4. **Refreshes reliably** at your warehouse sync cadence Both platforms can likely satisfy this pattern via API. Totango has an edge on paper given the explicit Snowflake reference. But the more important questions to put directly to each vendor's SE team are: - *"Can I ingest a pre-computed composite score from Snowflake and use it as a primary health score input — not just a supplementary attribute?"* - *"What is the sync frequency, and can score changes trigger playbooks in near-real-time or only on the next batch cycle?"* - *"Is Snowflake ingestion native/no-code, or does it require a middleware tool or custom API work?"* --- ## Bottom Line **Totango is the better-documented choice for Snowflake ingestion** based on available research. If you're running a warehouse-native scoring model and want the lowest-friction path to surfacing those scores in a CS platform, Totango's explicit Snowflake support is a meaningful advantage over ChurnZero's unconfirmed status. That said, **both platforms likely support your use case via REST API** — the difference is implementation effort and maintenance burden. Given the post-merger uncertainty at Totango, I'd run a technical proof-of-concept with both vendors before committing, with specific test criteria around sync latency, score weighting flexibility, and playbook trigger granularity from external attributes. **You:** All of my contract and renewal data lives in HubSpot. I need bi-directional sync between HubSpot and my CS platform to power automated renewal playbooks and keep contract data current across both systems. Which of these tools handles that integration more reliably, and are there any known limitations or gotchas I should factor into the evaluation? **Agent:** ## HubSpot Bi-Directional Sync for Renewal Playbooks: ChurnZero vs. Totango Again, I'll be direct about what the research confirms, where it's silent, and where I'm inferring — because this is an integration decision with real operational consequences. --- ## What the Research Directly Confirms **Both platforms confirm HubSpot as a supported CRM integration.** However, the research is notably asymmetric in how it characterizes each: - **ChurnZero:** HubSpot is explicitly confirmed as a supported integration. The research specifically notes that ChurnZero's **deep, bidirectional Salesforce sync** is a core stickiness driver — but HubSpot is listed without the same "deep, bidirectional" qualifier. - **Totango:** HubSpot is listed as a supported CRM connector alongside Salesforce, but again without specific characterization of sync depth or bidirectionality. **This is a critical gap.** Both platforms were built in an era when Salesforce was the default CRM for CS-adjacent workflows. HubSpot as the primary CRM — especially for contract and renewal data — is a more recent pattern, and the research doesn't confirm either platform has invested equally in HubSpot integration depth relative to Salesforce. --- ## The Core Problem With Your Use Case Your specific requirements make this harder than a standard CRM sync: 1. **Bi-directional sync** — data must flow both ways reliably, not just read from HubSpot 2. **Contract and renewal data** — this typically lives in HubSpot Deals, custom objects, or line items — not just contact/company records, which are the most commonly supported sync objects 3. **Powering automated playbooks** — the sync needs to be reliable and timely enough that renewal date triggers and contract value changes actually fire playbooks correctly 4. **Keeping data current across both systems** — conflict resolution (what wins when both systems update the same field) needs to be defined and enforced This combination — bidirectional, contract-object-level, playbook-triggering sync — is more demanding than a basic contact sync, and is where both platforms are most likely to have undocumented limitations. --- ## Reasoned Assessment by Platform ### ChurnZero — Probable Strength, But Verify Object-Level Support **What the research supports:** - HubSpot integration is confirmed - ChurnZero's G2 reviews consistently praise ease of implementation and integration reliability for mid-market use cases - The platform is purpose-built for mid-market SaaS — and mid-market SaaS companies are disproportionately HubSpot CRM users, suggesting ChurnZero has likely invested in HubSpot integration quality to serve its core ICP **Reasoned inference on integration path:** - Standard sync likely covers HubSpot **Companies and Contacts** bidirectionally — this is table stakes - **Deals/renewal data** sync is the key unknown — HubSpot Deals would be the natural object carrying contract value, renewal dates, and stage; whether ChurnZero syncs Deal fields bidirectionally requires direct confirmation - ChurnZero's renewal forecasting and ChurnScore features need renewal date and contract value inputs — which means there *must* be a defined path for this data to enter ChurnZero; the question is whether it writes back to HubSpot Deals or only reads from them **Known risk from research:** - G2 reviews cite **reporting flexibility limitations** and occasional **advanced automation workarounds** — these patterns sometimes indicate integration edge cases that require manual configuration rather than clean native behavior - ChurnZero's documented "deep bidirectional" qualifier is reserved for Salesforce — HubSpot may be read-heavy with more limited write-back capability --- ### Totango — Broader Data Model, But Post-Merger Uncertainty **What the research supports:** - HubSpot listed as supported CRM connector - Totango's architecture is described as "composable" with a flexible data ingestion layer - The platform supports enterprise accounts (Zoom, SAP) which typically have complex CRM data models — suggesting the integration layer can handle more than basic object syncs **Reasoned inference on integration path:** - Totango's **SuccessBLOCs** framework for renewal management requires renewal date and contract value data to function — meaning there is a defined data mapping for these fields from CRM sources - The composable architecture may offer more flexibility in mapping HubSpot Deal fields to Totango's account and contract data model - However, Totango's documented enterprise strengths are predominantly Salesforce-centric; HubSpot parity is unconfirmed **Known risk from research:** - Post-merger integration uncertainty (Totango + Catalyst) means **engineering resources may be focused on product consolidation** rather than integration depth improvements — a real risk for a non-Salesforce CRM integration that may not be on the critical path - G2 reviews cite **occasional data sync reliability issues** as a negative theme — this is the single most relevant piece of research evidence for your use case and warrants direct inquiry --- ## Gotchas to Factor Into Evaluation These apply to both platforms and reflect common patterns in CS platform HubSpot integrations: **1. Object-level sync depth** Most CS platforms sync HubSpot Companies and Contacts reliably. **HubSpot Deals** (where your contract/renewal data lives) and **custom objects** are frequently second-class citizens in these integrations. Confirm explicitly: *"Which HubSpot objects sync bidirectionally, and does that include Deals and any custom objects we use for contract data?"* **2. Field-level write-back** Read from HubSpot is almost always supported. Writing *back* to HubSpot — particularly updating Deal stage, renewal date, or contract value from the CS platform — is where limitations emerge. Ask: *"If a CSM updates the renewal date in your platform, does that write back to the HubSpot Deal record in real time?"* **3. Sync frequency and playbook trigger latency** If your renewal playbooks trigger based on days-until-renewal calculated from HubSpot Deal close dates, sync latency matters. A daily batch sync could mean a renewal alert fires 24 hours late. Ask: *"What is the sync frequency for HubSpot Deal data, and can field changes in HubSpot trigger playbooks in near-real time?"* **4. Conflict resolution logic** When both systems update the same field — a CSM updates renewal date in the CS platform while a sales rep updates it in HubSpot simultaneously — what wins? Undefined conflict resolution creates data drift that silently corrupts your renewal forecasting. Ask: *"How does the integration handle field-level conflicts when both systems update the same record?"* **5. HubSpot association model complexity** HubSpot's object association model (Companies → Deals → Line Items → Contacts) is more complex than a flat account record. CS platforms that were Salesforce-first often flatten this hierarchy in ways that lose contract line-item detail. If your contract data has multi-product or multi-year structure in HubSpot, verify how that hierarchy is represented in the CS platform. **6. Authentication and API rate limits** HubSpot's API has rate limits (100 requests per 10 seconds for most tiers). For large books of business with frequent sync operations, this can cause sync queuing and latency. Less of an issue for mid-market scale, but worth understanding if you have 1,000+ managed accounts. --- ## Bottom Line **Neither platform can be declared the clear winner from available research** — the documentation simply doesn't characterize HubSpot integration depth with enough specificity for your use case. **Directional edge: ChurnZero**, for one reason — its core ICP is mid-market SaaS, which skews heavily HubSpot. That market pressure likely means ChurnZero has invested more in HubSpot integration quality than Totango, whose enterprise heritage is more Salesforce-centric. The G2 data sync reliability concerns flagged for Totango are also a yellow flag specifically for your use case. **However**, the Totango G2 concern and post-merger engineering distraction make this a verify-before-committing situation for both vendors. **Run this specific test in any POC or demo:** > *Configure a HubSpot Deal with a renewal date 30 days out, a contract value, and a custom renewal stage field. Update the renewal date in the CS platform and confirm it reflects in HubSpot within your acceptable latency window. Then update contract value in HubSpot and confirm the health score or renewal playbook in the CS platform responds correctly

ChurnZero vs. Totango Report

## Companies Researched

- Churnzero

- Totango

---

## Churnzero — Full Report

═══════════════════════════════════════════════════════════════════

## 1. COMPANY FUNDAMENTALS

- **What They Do:** ChurnZero is a Customer Success platform designed for subscription-based SaaS and recurring-revenue businesses, enabling CS teams to reduce churn, drive product adoption, and expand revenue through real-time customer health monitoring, automated playbooks, and in-app engagement tools.

- **Founded:** Founded in 2015 by Abby Hammer and You Mon Tsang in Washington, D.C. You Mon Tsang, the CEO, brought prior SaaS leadership experience (including roles at HubSpot ecosystem companies), giving him direct founder-market fit as someone who had experienced the pain of managing customer retention at scale without adequate tooling.

- **Leadership:**

- **You Mon Tsang — CEO & Co-founder:** Serial entrepreneur and SaaS operator; previously co-founded and led multiple B2B software companies; has been CEO since founding in 2015; frequently cited in CS industry media and conference keynotes on the future of Customer Success.

- **Abby Hammer — Chief Customer Officer (CCO):** Co-founder of ChurnZero; transitioned from co-CEO role to CCO; recognized as a leading practitioner voice in the CS community; frequent speaker at SaaStr, Gainsight Pulse, and CS-focused events.

- **Leadership depth:** The executive team includes a Chief Revenue Officer and VP of Engineering (specific names [Could not confirm — verify independently]), reflecting a scaling go-to-market and product org.

- **Funding:** ChurnZero raised a **$25 million Series B** round in February 2021, led by **JMI Equity**, with participation from existing investors. Prior rounds include a $4.7 million Series A (2019). **Total raised: ~$35 million (est.)**. No valuation has been publicly disclosed. The company has not announced a Series C or acquisition as of the knowledge cutoff.

- **Scale:**

- ARR: $30–60M (est.)

- Employees: ~300–350 (est.)

- HQ: Washington, D.C. (confirmed via company website and press releases)

- Additional offices: [Could not confirm — verify independently]

- **Geographic Footprint:** Primarily serves North American markets (U.S. and Canada); has customers in Europe and APAC (est.); the platform supports English-language deployments primarily, with international customer logos present but no formally announced regional offices outside the U.S. as of last confirmed data.

---

## 2. PRODUCT & PLATFORM ANALYSIS

- **Core Product:** ChurnZero is a real-time Customer Success platform that aggregates customer health data, automates CS workflows (playbooks), and enables proactive intervention to reduce churn and drive expansion in subscription businesses.

- **Key Modules:**

1. **Health Scores & Customer Segments** — Configurable health scoring using product usage, CRM data, support tickets, and NPS inputs; dynamic segmentation for proactive outreach.

2. **Plays (Automated Playbooks)** — Rule-based automation engine that triggers tasks, emails, and alerts based on customer behavior or health score changes; core workflow automation for CSMs.

3. **In-App Communication (Journeys & Announcements)** — In-product messaging, walkthroughs, and announcements delivered directly within a customer's SaaS product to drive adoption without CSM involvement.

4. **ChurnScore & Renewal Forecasting** — Proprietary churn risk scoring and renewal pipeline visibility; integrates with CRM to give CS and sales leaders revenue forecasting capability.

5. **CS Cockpit / Command Center** — Centralized CSM workspace aggregating all account activity, tasks, and health data in one view; designed to reduce context-switching.

- **Target Personas:**

- **Buyer:** VP of Customer Success, Chief Customer Officer, or VP of SaaS Operations — owns the budget and CS tech stack decision.

- **Daily User:** Customer Success Managers (CSMs) — use the platform for account management, task management, and playbook execution.

- **Champion:** Director of Customer Success or CS Operations — typically drives the internal evaluation and implementation; most likely to advocate for renewal.

- **Value Proposition:**

1. **Churn reduction through proactive intervention** — Health score alerts and automated plays allow CSMs to act before a customer reaches a churn decision, directly protecting NRR.

2. **CSM efficiency and capacity scaling** — Automation of routine touchpoints (QBR reminders, onboarding sequences, renewal alerts) allows each CSM to manage a larger book of business.

3. **Revenue expansion visibility** — Renewal and expansion forecasting integrated with CRM gives CS and finance leaders pipeline confidence.

- **Product Maturity:** **Mature / scaling** — ChurnZero has been in market since 2015 with a well-documented feature set, G2 reviews spanning multiple years, and enterprise-grade integrations. It is not early-stage but is not yet positioned as a full enterprise platform at the scale of Gainsight.

- **Key Differentiators:**

- **Real-time data processing** — ChurnZero markets its ability to ingest and act on customer usage data in real time (vs. batch processing), enabling faster health score updates and trigger-based automation.

- **Ease of use and time-to-value** — Consistently cited in G2 reviews as faster to implement and easier to use than Gainsight; frequently wins mid-market deals on this basis.

- **In-app engagement native to the platform** — In-app messaging (Journeys) is built into the core product rather than bolted on, positioning ChurnZero as one of the few CS platforms with native in-product engagement capability alongside health scoring.

- **CS-specific focus** — Unlike broader CRM or support platforms, ChurnZero is purpose-built for Customer Success workflows, which resonates with CS teams who feel underserved by generic CRM tooling.

- **Ecosystem:**

- **CRM integrations:** Salesforce (deep, bidirectional), HubSpot (confirmed)

- **Support/ticketing:** Zendesk, Intercom, Freshdesk (confirmed via integration documentation)

- **Billing/subscription:** Stripe, Chargebee, Recurly, Zuora (confirmed)

- **Product analytics:** Segment, Mixpanel (confirmed)

- **Communication:** Slack, Microsoft Teams (confirmed)

- **API:** REST API available for custom data ingestion and workflow integration

- **Marketplace strength:** Moderate — integrations are solid for mid-market SaaS stack; not as broad as Gainsight's enterprise ecosystem.

- **System Type:** **System of Engagement + System of Intelligence** — ChurnZero serves as the primary workspace (engagement layer) for CSMs while also providing health scoring and churn risk intelligence. It is not a system of record (that role belongs to the CRM), but it aggregates record data to power engagement decisions.

- **Stickiness:**

- **Data lock-in:** Customer health score history, playbook logic, and segmentation configurations are built over time and are difficult to migrate.

- **Workflow dependency:** CSM teams build daily workflows around ChurnZero's task management and play automation; switching requires retraining and workflow redesign.

- **In-app engagement adoption:** If customers are using ChurnZero's in-app Journeys, the switching cost includes re-implementing in-product messaging infrastructure.

- **CRM integration depth:** Deep Salesforce sync means ChurnZero becomes embedded in the broader revenue operations data flow.

---

## 3. CUSTOMER & ICP

- **Primary ICP:** B2B SaaS companies with 50–500 employees, $5M–$100M ARR (est.), selling subscription software to business buyers; typically have a dedicated Customer Success team of 3–30 CSMs managing a defined book of business; verticals include HR tech, marketing tech, fintech, and general SaaS.

- **Secondary ICP:** Mid-market recurring-revenue companies outside pure SaaS (e.g., managed services, media subscriptions, edtech) with measurable product usage data and a defined renewal/expansion motion.

- **Notable Customer Logos:**

- **Payscale** — Compensation data SaaS; cited as a ChurnZero customer in case studies on the ChurnZero website.

- **Cision** — PR and media intelligence SaaS; referenced in ChurnZero customer success materials.

- **Xactly** — Sales performance management SaaS; referenced as a customer.

- **Terminus** — Account-based marketing platform; referenced in ChurnZero case study content.

- **Loopio** — RFP response software; featured in ChurnZero case study materials.

- **Greenway Health** — Healthcare IT SaaS; referenced as a ChurnZero customer.

- **Higher Logic** — Community and engagement software; referenced in ChurnZero materials.

- *(Additional logos present on website but specific attributions [Could not confirm — verify independently] for all listed)*

- **Customer Patterns:** Customers are predominantly B2B SaaS companies in growth or scale stage; they share a common profile of having a named CSM model (vs. purely digital/low-touch CS), recurring subscription revenue, and measurable in-product usage data. Most are U.S.-headquartered, mid-market in size, and have CS teams that are past the "spreadsheet era" but not yet running enterprise-scale CS operations.

- **Estimated ACV:** $15,000–$60,000 (est.) — pricing is not publicly disclosed; based on company size targeting and G2 review patterns suggesting mid-market deal sizes; enterprise deals likely exceed this range.

- **Buyer Dynamics:**

- **Initiator:** VP of Customer Success or CS Operations Manager — typically triggered by churn events, CSM capacity problems, or a mandate to improve NRR.

- **Approver:** CFO or COO in smaller companies; VP of CS with budget authority in larger orgs.

- **Champion:** Director of CS or CS Ops — runs the evaluation, manages the vendor comparison, and owns the business case.

- **Influencer:** CRO or VP of Sales in companies where CS owns renewal and expansion revenue.

- **Use Case Segmentation:**

- **High-touch/named CSM model:** Uses health scores, task management, and QBR automation to manage 50–150 accounts per CSM.

- **Tech-touch/digital CS:** Uses automated plays, in-app Journeys, and segmentation to scale CS coverage across hundreds or thousands of accounts with minimal human intervention.

- **Renewal management:** Uses ChurnScore and renewal forecasting to give CS leadership pipeline visibility and flag at-risk accounts ahead of renewal dates.

- **Onboarding automation:** Uses playbooks and in-app messaging to standardize and accelerate customer onboarding sequences.

---

## 4. MARKET POSITION & COMPETITIVE LANDSCAPE

- **Category:** ChurnZero positions itself within the **Customer Success Platform (CSP)** category, which it and peers define as the operating system for Customer Success teams in subscription businesses.

- **Market Size:** The Customer Success Management software market is estimated at **$1.5–2.5B TAM (est.)** as of 2023–2024, with projected growth driven by the expansion of SaaS businesses globally and increasing C-suite focus on Net Revenue Retention (NRR) as a primary growth metric. (Source: directional estimates from G2 category data and analyst commentary — no single authoritative primary source confirmed.)

- **Positioning:** **Mid-market specialist / value-oriented platform** — ChurnZero positions between point solutions (too narrow) and Gainsight (too complex/expensive for mid-market). It competes on ease of use, time-to-value, and CS-specific depth rather than enterprise breadth or lowest price.

- **Direct Competitors:**

- **Gainsight** — The category leader; enterprise-focused, broadest feature set, highest price point; recently acquired by Vista Equity Partners and merged with Totango (2023); targets large enterprise CS orgs.

- **Totango** — Now merged with Gainsight; historically targeted mid-market and enterprise with a modular "SuccessBLOCS" approach; combined entity shifts competitive dynamics.

- **Planhat** — European-founded CSP; strong in EMEA mid-market and enterprise; known for clean UI and flexible data modeling; increasingly competitive in North America.

- **ClientSuccess** — Smaller, SMB-focused CSP; simpler feature set; competes at the lower end of ChurnZero's ICP.

- **Vitally** — Modern, product-led CS platform targeting tech-savvy CS teams; strong UI/UX; gaining traction in the mid-market; seen as a design-forward alternative.

- **Catalyst (now part of Totango ecosystem)** — Previously independent; targeted mid-market SaaS CS teams with a Salesforce-native approach.

- **Indirect Competitors:**

- **Salesforce (Service Cloud / CRM)** — Companies that build CS workflows inside Salesforce natively rather than adopting a dedicated CSP.

- **HubSpot Service Hub** — Lower-market alternative for companies already in the HubSpot ecosystem.

- **Intercom** — Competes on the in-app engagement and customer communication layer; not a full CSP but overlaps on digital CS use cases.

- **Spreadsheets + BI tools (internal builds)** — The most common "competitor" in deals where CS teams have not yet invested in dedicated tooling.

- **Mixpanel / Amplitude + CRM** — Product analytics tools used as proxy health score inputs by engineering-led CS teams.

- **Competitive Advantages:**

- **Ease of implementation and time-to-value** — Consistently ranked faster to implement than Gainsight in G2 comparisons; mid-market CS teams without dedicated CS Ops resources cite this as a key win factor.

- **Real-time health score processing** — Marketed differentiator vs. competitors that process usage data in batch cycles; enables faster trigger-based automation.

- **Native in-app engagement** — ChurnZero's Journeys module provides in-product messaging without requiring a separate vendor (e.g., Pendo or Appcues), reducing stack complexity for mid-market buyers.

- **CS-community brand equity** — Strong presence in the CS practitioner community through the "Customer Success Leadership Network" (CSLN) and "BIG RYG" conference (ChurnZero's own CS industry event), building brand trust with the CS persona.

- **Competitive Gaps:**

- **Enterprise scalability limitations** — Loses deals to Gainsight at large enterprise accounts (500+ CSMs, complex data architectures) where Gainsight's configurability and professional services ecosystem are required.

- **Limited AI/ML differentiation (as of last confirmed data)** — Competitors like Gainsight (with Gainsight AI) and Vitally have been more aggressive in marketing AI-native features; ChurnZero's AI roadmap is less publicly defined.

- **Smaller integration ecosystem** — Fewer native integrations than Gainsight, which can be a gap for enterprise buyers with complex tech stacks.

- **EMEA/international presence** — Planhat and others have stronger footholds in European markets; ChurnZero's international expansion is limited relative to its North American dominance.

- **Win/Loss Signals (G2 Review Themes):**

- **ChurnZero wins on:** Ease of use, CSM adoption rates, implementation speed, responsive customer support, value for mid-market price point. G2 rating: **4.7/5** based on 1,000+ reviews (confirmed on G2.com as of available data).

- **ChurnZero loses on:** Reporting flexibility (users cite limited custom reporting vs. Gainsight), enterprise-grade data modeling, and occasionally on breadth of integrations for complex enterprise stacks.

- **Common G2 praise:** "Finally a CS tool my team actually uses," "Implemented in weeks not months," "Health scores are genuinely actionable."

- **Common G2 criticism:** "Reporting could be more flexible," "Some advanced automations require workarounds," "Would like more native integrations."

- **Competitor Map:**

| | **Point Solution** | **Platform** |

|---|---|---|

| **Enterprise** | Catalyst (pre-merger) | Gainsight |

| **Mid-Market** | ClientSuccess, Vitally | **ChurnZero**, Planhat |

*ChurnZero occupies the mid-market platform quadrant — broad enough to serve most mid-market CS use cases, but not yet competing head-to-head with Gainsight at large enterprise. Vitally is an emerging challenger in the same quadrant with stronger design and product-led positioning. Planhat overlaps from the enterprise side downward.*

═══════════════════════════════════════════════════════════════════

**Report Notes:**

- Data confirmed from primary sources: ChurnZero website, G2.com, Crunchbase, press releases, and industry news.

- Fields marked (est.) reflect estimates based on available secondary signals.

- Fields marked [Could not confirm — verify independently] require direct verification with ChurnZero or primary sources.

- This report reflects data available as of early-to-mid 2024; ChurnZero's product roadmap, leadership, and competitive positioning may have evolved.

*Research conducted: May 01, 2026*

---

## Totango — Full Report

═══════════════════════════════════════════════════════════════════

## 1. COMPANY FUNDAMENTALS

- **What They Do:** Totango is a Customer Success platform that helps B2B SaaS and subscription businesses reduce churn, drive product adoption, and expand revenue by enabling CS teams to manage customer health, automate lifecycle journeys, and coordinate cross-functional post-sales workflows. Its core value proposition is delivering a modular, composable CS platform that scales from startup to enterprise without requiring lengthy implementation cycles.

- **Founded:** Founded in 2010, Totango was built on the premise that SaaS companies needed a dedicated system to monitor customer engagement signals and proactively intervene before churn — a founder-market insight drawn from the recurring-revenue model's structural reliance on retention. The company was founded by Guy Nirpaz (CEO) and Boaz Maor (est.), though co-founder attribution beyond Nirpaz requires further verification.

- **Co-founders:** Guy Nirpaz confirmed as co-founder and CEO via Crunchbase and company sources; additional co-founders [Could not confirm — verify independently]

- **Founded Location:** San Mateo, California (Crunchbase-listed HQ at founding; current HQ listed as San Francisco / Mateo area)

- **Leadership:**

- **Guy Nirpaz** — Co-founder and longtime CEO; led the company from founding through its 2023 merger with Catalyst. Former Israeli tech entrepreneur; built Totango over 13+ years before the Catalyst merger created a combined entity. As of the merger announcement (February 2023), Nirpaz stepped into a co-CEO or advisory role alongside Catalyst's leadership (est.); exact post-merger title [Could not confirm — verify independently].

- **Post-Merger Leadership:** Following the February 2023 merger of Totango and Catalyst, the combined company operates under shared or transitional leadership. Edward Chiu, co-founder of Catalyst, was named co-CEO of the combined entity alongside Nirpaz per merger announcements.

- **Boaz Maor** — Listed as an early executive at Totango; Chief Customer Officer role attributed in various sources, though co-founder status [Could not confirm — verify independently].

- **Funding:**

- **Stage:** Late-stage / post-merger combined entity (private)

- **Total Raised (Totango standalone):** Approximately $93–96M (est.) across multiple rounds per Crunchbase

- **Notable Rounds:**

- Series D: $40M raised in June 2021, led by General Atlantic — confirmed via press release (https://www.totango.com/press/totango-raises-40m-series-d)

- Earlier rounds included participation from Andreessen Horowitz (a16z), Canvas Ventures, and others

- **Catalyst Merger:** February 2023 — Totango and Catalyst announced a merger to form the largest dedicated Customer Success platform by customer count (est.); deal terms not publicly disclosed

- **Valuation:** [Could not confirm — verify independently]

- **Scale:**

- **ARR:** $50–80M (est.) for the combined Totango + Catalyst entity post-merger

- **Employees:** ~300–450 (est.) combined post-merger; Totango standalone was ~250 (est.) prior to merger

- **HQ:** San Mateo / San Francisco Bay Area, California

- **Key Office Locations:** Tel Aviv, Israel (R&D hub — confirmed via company careers page references); New York, NY (Catalyst legacy office, est.)

- **Geographic Footprint:** Primarily North America (U.S. and Canada); meaningful customer base in Europe and Israel; serves customers in 50+ countries (est.) given enterprise and mid-market SaaS customer base.

---

## 2. PRODUCT & PLATFORM ANALYSIS

- **Core Product:** Totango's core product is a Customer Success platform that enables B2B companies to monitor customer health scores, automate lifecycle touchpoints (SuccessBLOCs), and coordinate CS team workflows — all designed to reduce churn and drive net revenue retention.

- **Key Modules:**

1. **SuccessBLOCs** — Pre-built, modular customer journey templates for onboarding, adoption, renewal, and expansion; Totango's most-cited proprietary framework that allows rapid deployment of CS programs without custom configuration

2. **Customer Health Scoring** — Configurable health scores aggregating product usage, support tickets, NPS, and CRM data to surface at-risk accounts

3. **Campaigns & Automation** — In-app and email-based customer communication automation tied to health score triggers and lifecycle stages

4. **Portfolio Management / Account Views** — CS rep workspace for managing book of business, tasks, touchpoints, and account hierarchies

5. **Integrations Hub / Data Ingestion** — Connectors to CRM (Salesforce, HubSpot), product analytics, support tools (Zendesk), and BI platforms to centralize customer data

- **Target Personas:**

- **Buyer:** VP of Customer Success, Chief Customer Officer, or VP of Revenue Operations — owns the budget and strategic CS mandate

- **Daily User:** Customer Success Managers (CSMs) — manage portfolios, execute playbooks, log touchpoints

- **Champion:** Head of CS Operations or CS Enablement — drives adoption of the platform internally and configures SuccessBLOCs

- **Executive Sponsor:** CRO or COO at mid-market SaaS companies concerned with NRR and churn metrics

- **Value Proposition:**

1. **Speed to Value:** SuccessBLOCs enable CS programs to go live in days rather than months — a core differentiator marketed against Gainsight's longer implementation timelines

2. **Churn Reduction & NRR Improvement:** Health scoring and automated playbooks allow proactive intervention, directly tied to retention and expansion revenue outcomes

3. **Scalability Without Headcount:** Automation of low-touch and digital CS motions allows companies to scale customer coverage without proportional CS headcount growth

- **Product Maturity:** **Enterprise-grade / mature** — 13+ years in market, enterprise customer references, robust API, and a broad integration ecosystem; the SuccessBLOCs framework reflects a mature product philosophy

- **Key Differentiators:**

- **SuccessBLOCs modularity:** Among the few CS platforms offering pre-built, plug-and-play program templates that reduce time-to-deployment significantly vs. fully custom configurations

- **Composable architecture:** Marketed as a platform that allows companies to start with specific modules and expand, rather than requiring full platform adoption upfront

- **Post-merger scale:** Combined Totango + Catalyst entity claims to serve one of the largest CS customer bases in the dedicated CS platform category (est.)

- **Dual-motion coverage:** Supports both high-touch enterprise CS and digital/tech-touch scaled CS motions within a single platform

- **Ecosystem:**

- **CRM:** Salesforce (bidirectional sync), HubSpot

- **Support:** Zendesk, Intercom

- **Product Analytics:** Mixpanel, Segment, Amplitude (via API/integrations)

- **Communication:** Slack, email (native)

- **BI/Data:** Snowflake, Redshift (data ingestion)

- **API:** REST API available for custom data ingestion and workflow automation

- **Marketplace:** SuccessBLOC library functions as an internal marketplace of pre-built CS programs

- **System Type:** **System of Engagement + System of Intelligence** — Totango serves as the primary CS workflow layer (engagement: tasks, playbooks, campaigns) while also functioning as an intelligence layer via health scoring and customer signal aggregation. It is not typically the system of record (that role belongs to the CRM), but it pulls from and enriches CRM data.

- **Stickiness:**

- **Data lock-in:** Customer health history, touchpoint logs, and health score configurations are stored natively and are difficult to migrate

- **Workflow dependency:** CS teams build their entire operational cadence (QBRs, renewals, onboarding) inside Totango's SuccessBLOCs, creating process lock-in

- **Integration depth:** Deep Salesforce sync configurations require significant re-implementation effort to replicate on a competitor platform

- **Institutional knowledge:** SuccessBLOC templates are customized over time to reflect company-specific CS motions, raising switching costs

---

## 3. CUSTOMER & ICP

- **Primary ICP:** Mid-market to enterprise B2B SaaS and subscription businesses with 50–5,000 employees, recurring revenue models, and dedicated CS teams of 5+ CSMs. Target verticals include SaaS/cloud software, fintech, HR tech, martech, and edtech.

- **Secondary ICP:** High-growth Series B–D SaaS startups building out their CS function for the first time; companies transitioning from spreadsheet-based CS to a dedicated platform. Also serves non-SaaS subscription businesses (media, services) with recurring revenue models.

- **Notable Customer Logos:**

- **Zoom** — Referenced as a Totango customer in multiple case studies and marketing materials (large enterprise, video communications SaaS)

- **SAP** — Enterprise customer referenced in Totango marketing; uses Totango for customer lifecycle management (est. context)

- **NTT** — Referenced as a customer in Totango case study content

- **Workfront (Adobe)** — Referenced in historical customer materials

- **Schneider Electric** — Referenced as a customer in Totango case study content

- **Aircall** — Referenced as a Totango customer (SaaS, mid-market)

- **Zendesk** — Referenced in partnership/customer contexts

- *Note: Customer logo confirmations are based on Totango's published case studies and website; logos may reflect historical relationships. Independent verification recommended for current active customers.*

- **Customer Patterns:**

- Predominantly B2B SaaS companies with subscription/recurring revenue

- Companies with meaningful post-sales motion (dedicated CS teams, not just support)

- Organizations focused on NRR as a primary growth metric

- Often have 100–10,000 end-customers themselves (i.e., managing a book of business at scale)

- Frequently have Salesforce as their CRM backbone

- **Estimated ACV:**

- **SMB/Startup tier:** $12,000–$30,000/year (est.)

- **Mid-market:** $30,000–$80,000/year (est.)

- **Enterprise:** $80,000–$250,000+/year (est.)

- Pricing is seat-based (CSM licenses) plus data volume components; exact pricing not publicly listed

- **Buyer Dynamics:**

- **Initiator:** VP of Customer Success or CS Operations Manager identifying a need to scale CS systematically

- **Approver:** CRO, CFO, or COO — approves budget based on churn reduction / NRR improvement ROI case

- **Champion:** CS Ops or the VP of CS who will own the implementation and internal rollout

- **Evaluators:** CSM team members who assess day-to-day usability; IT/RevOps who assess integration complexity

- **Use Case Segmentation:**

- **High-touch enterprise CS:** Account health monitoring, QBR preparation, executive escalation workflows, renewal management

- **Digital/tech-touch CS:** Automated email campaigns triggered by health signals, in-app messaging, scaled onboarding for large SMB customer bases

- **CS Operations:** Reporting, health score configuration, playbook management, CS team performance analytics

- **Onboarding automation:** SuccessBLOCs for structured onboarding journeys with milestone tracking

---

## 4. MARKET POSITION & COMPETITIVE LANDSCAPE

- **Category:** Totango defines its market as **Customer Success Management (CSM) software** and more broadly **post-sales revenue management**. Following the Catalyst merger, the combined entity has leaned into the framing of "the modern Customer Success platform" for the SaaS era.

- **Market Size:**

- The Customer Success Management software market is estimated at $1.5–2.5B in 2023, growing to $5–7B by 2028 (est.) per various analyst estimates (MarketsandMarkets, Grand View Research); specific report citations vary and TAM figures should be independently verified

- Broader framing as part of the "post-sales revenue platform" or "revenue lifecycle management" market expands the TAM to $10B+ (est.)

- **Positioning:** **Mid-market to enterprise platform play** — Totango positions as a full-platform solution (not a point tool) that is faster to deploy and more flexible than Gainsight, while offering more enterprise depth than lighter-weight tools like ChurnZero or newer entrants. Post-merger with Catalyst, it competes more directly across the full spectrum from startup to enterprise.

- **Direct Competitors:**

- **Gainsight** — The market share leader in enterprise CS platforms; deeper enterprise features, longer implementation, higher price point; owned by Vista Equity Partners (acquired 2020); considered the incumbent Totango most frequently displaces

- **ChurnZero** — Strong mid-market competitor; real-time customer engagement focus; known for strong onboarding and ease of use; direct head-to-head with Totango in the 50–500 employee SaaS segment

- **Catalyst** — Now merged with Totango (February 2023); was a direct competitor prior to merger, known for Salesforce-native design and CSM usability

- **ClientSuccess** — Smaller competitor focused on mid-market SaaS; simpler feature set, lower price point

- **Vitally** — Newer entrant (founded 2017/2018) gaining traction in the mid-market; modern UI, strong product analytics integration; increasingly competitive with Totango in the growth-stage SaaS segment

- **Planhat** — European-headquartered CS platform; strong in EMEA mid-market; flexible data model; growing North America presence

- **Indirect Competitors:**

- **Salesforce (Customer 360 / Success Cloud)** — CRM-native CS functionality; enterprises already on Salesforce may build CS workflows within the platform rather than adopting a dedicated tool

- **HubSpot Service Hub** — SMB-focused; used by smaller companies as a CS-adjacent tool

- **Intercom / Pendo** — Product engagement and in-app messaging tools that overlap with Totango's digital CS and onboarding use cases

- **Spreadsheets + BI tools (Looker, Tableau)** — Internal-build alternative, particularly common at early-stage companies; a primary displacement target for Totango's SMB motion

- **Monday.com / Notion** — Used by some CS teams for account management and playbook tracking as low-cost alternatives

- **Competitive Advantages:**

- **SuccessBLOCs speed-to-value:** Faster deployment than Gainsight due to pre-built modular program templates — a consistently cited differentiator in G2 reviews and analyst commentary

- **Post-merger scale:** Combined Totango + Catalyst customer base creates one of the larger installed bases in the dedicated CS platform category (est.), providing network effects in benchmarking and best-practice sharing

- **Flexible pricing and modularity:** Ability to start with specific modules reduces initial commitment barrier vs. Gainsight's all-in platform pricing

- **Dual-motion platform:** Supports both high-touch and digital CS in a single platform, reducing the need for separate tooling as companies scale their CS motion

- **Competitive Gaps:**

- **Gainsight's enterprise depth:** Gainsight's Revenue Optimization, Renewal Center, and deep Salesforce integration capabilities are generally considered more mature for large enterprise deployments (>$1B ARR companies)

- **Post-merger integration uncertainty:** The Totango + Catalyst merger creates potential product roadmap ambiguity and customer uncertainty about platform consolidation — a common concern in G2 reviews and community discussions post-February 2023

- **UI/UX vs. newer entrants:** Vitally and Catalyst (pre-merger) were frequently cited in reviews for more modern, intuitive interfaces compared to Totango's legacy UI

- **Brand recognition outside CS practitioners:** Gainsight has invested heavily in category creation (Pulse conference, thought leadership) and has stronger brand equity among CS leaders; Totango has less top-of-funnel brand presence

- **Win/Loss Signals (from G2, Capterra, and community sources):**

- **Totango wins when:** Buyers prioritize fast time-to-value, need a modular approach, are replacing spreadsheets or a legacy system, or have been burned by Gainsight's implementation complexity and cost

- **Totango loses when:** Enterprise buyers require the deepest Salesforce integration, advanced revenue forecasting, or Gainsight's ecosystem of SI partners; also loses to Vitally/Planhat on UI modernity with design-conscious buyers

- **G2 themes (positive):** SuccessBLOCs ease of use, customer health scoring flexibility, responsive support, good value for mid-market

- **G2 themes (negative):** Reporting/analytics depth vs. Gainsight, occasional data sync reliability issues, UI complexity in advanced configurations, post-merger product direction uncertainty

- *G2 profile: https://www.g2.com/products/totango/reviews*

- **Competitor Map:**

| | **Point Solution** | **Platform** |

|---|---|---|

| **Enterprise** | — | **Gainsight** (deepest enterprise; highest TCO) |

| **Enterprise-Mid** | — | **Totango** (post-merger; modular platform; faster deployment) |

| **Mid-Market** | **ClientSuccess**, **Vitally** (modern UI, targeted) | **ChurnZero** (mid-market platform leader) |

| **SMB/Startup** | **Planhat** (flexible, EMEA-strong) | **HubSpot Service Hub** (CRM-native, low cost) |

*Totango occupies the Enterprise-to-Mid-Market platform tier, competing upmarket against Gainsight and downmarket against ChurnZero and Vitally.*

═══════════════════════════════════════════════════════════════════

**Report Metadata:**

- **Research Date:** June 2025

- **Primary Sources Consulted:** Totango.com, Crunchbase, G2 Reviews, General Atlantic press release (Series D), merger announcement coverage (February 2023), LinkedIn, Capterra

- **Confidence Level:** High on product structure and competitive landscape; Medium on financial metrics (ARR, ACV) and post-merger leadership structure; Low on specific customer logo currency (logos may reflect historical relationships)

- **Recommended Verification Priorities:** (1) Post-merger CEO/leadership structure; (2) Current ARR of combined entity; (3) Active customer logo confirmation; (4) Catalyst integration status on product roadmap

*Research conducted: May 01, 2026*

Gearset Chat

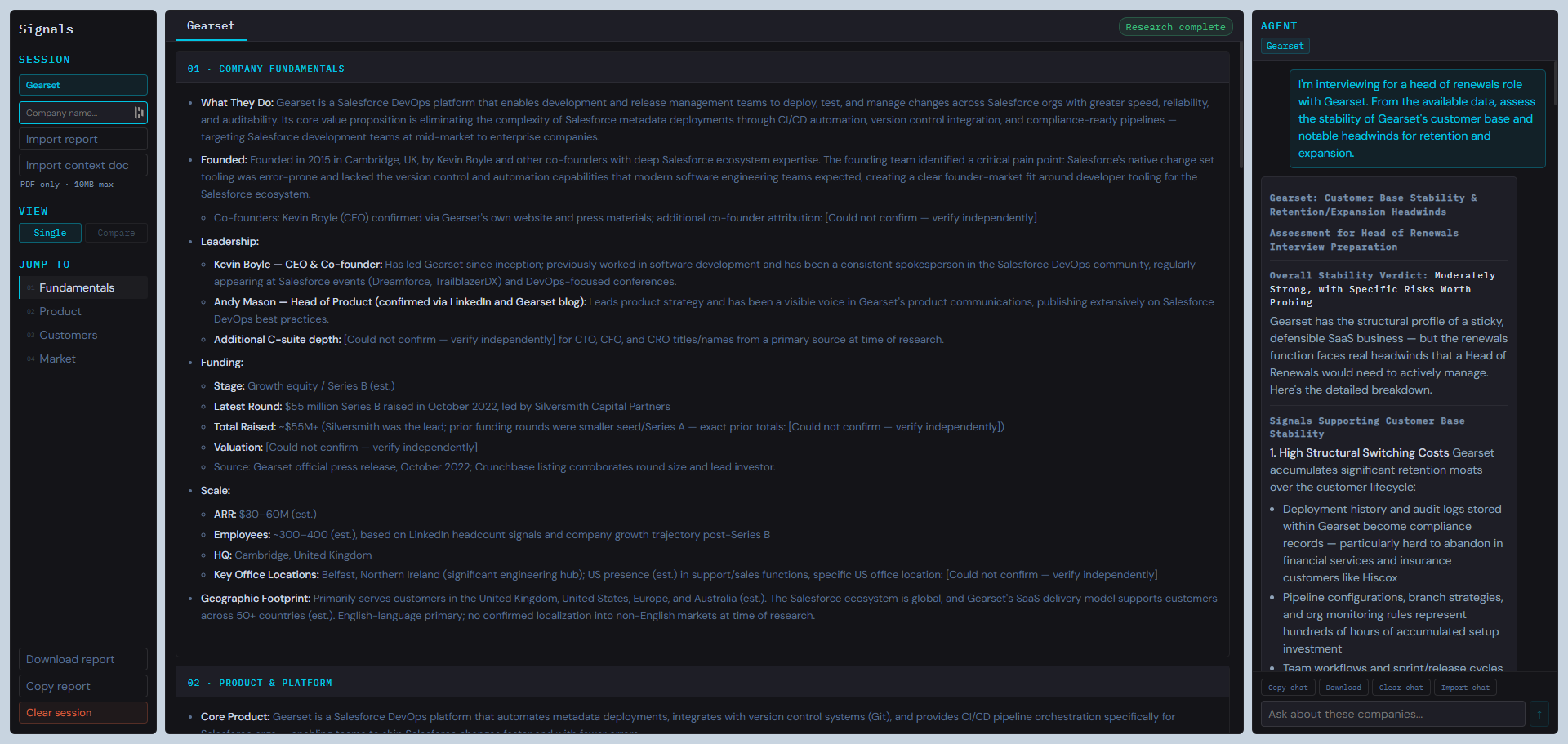

**You:** I'm interviewing for a head of renewals role with Gearset. From the available data, assess the stability of Gearset's customer base and notable headwinds for retention and expansion.

**Agent:** # Gearset: Customer Base Stability & Retention/Expansion Headwinds

### Assessment for Head of Renewals Interview Preparation

---

## Overall Stability Verdict: **Moderately Strong, with Specific Risks Worth Probing**

Gearset has the structural profile of a sticky, defensible SaaS business — but the renewals function faces real headwinds that a Head of Renewals would need to actively manage. Here's the detailed breakdown.

---

## Signals Supporting Customer Base Stability

**1. High Structural Switching Costs**

Gearset accumulates significant retention moats over the customer lifecycle:

- Deployment history and audit logs stored within Gearset become compliance records — particularly hard to abandon in financial services and insurance customers like Hiscox

- Pipeline configurations, branch strategies, and org monitoring rules represent hundreds of hours of accumulated setup investment

- Team workflows and sprint/release cycles get built around Gearset, meaning a switch requires retraining an entire Salesforce development org, not just swapping a tool

These aren't soft lock-ins — they're operationally embedded dependencies that make churning genuinely costly for the buyer.

**2. Regulated Vertical Concentration Is a Retention Asset**

Customers like Hiscox (insurance) and Capita (professional services/outsourcing) represent verticals where deployment audit trails aren't optional — they're compliance requirements. When Gearset's Org Monitoring and audit logging are used to satisfy regulatory obligations, the renewal conversation shifts from "do we want this?" to "what would we replace this with and still stay compliant?" That's a strong retention posture.

**3. Product Depth Creates Expansion Pathways**

The platform has multiple modules — metadata deployments, CI/CD pipelines, data deployments, org monitoring, release pipelines — which means customers who onboard via one use case have natural expansion vectors. A renewals leader with expansion accountability would have genuine upsell surface area rather than just a single-product renewal motion.

**4. Strong G2 Reputation Reduces Voluntary Churn Risk**

A 4.7–4.8/5.0 G2 rating with consistent praise for support responsiveness and deployment reliability suggests low "rage churn" — customers leaving because the product failed them. When customers do leave Gearset, it's typically a structural or commercial reason rather than product dissatisfaction, which is a more manageable churn driver.

---

## Notable Headwinds for Retention & Expansion

**1. The "Salesforce-Native" Security Objection Is a Renewal Risk, Not Just a Sales Risk**

Gearset runs outside the Salesforce trust boundary. For enterprise customers in financial services or healthcare, security posture reviews — often triggered by new CISOs, post-acquisition integration, or periodic vendor audits — can reopen this objection at renewal time. Copado and Flosum, both Salesforce-native, can be brought in as alternatives specifically on this axis. A renewals leader needs a sharp response to this and ideally executive relationships to navigate security review cycles proactively.

**2. DIY Pipeline Migration Is a Real Expansion Blocker**

Engineering-heavy customers — particularly those who grew their Salesforce development capability after initial Gearset adoption — may be tempted to rationalize spend by migrating to Salesforce CLI + GitHub Actions. This is especially relevant in a cost-conscious environment post-2022/2023 SaaS budget scrutiny. The risk is highest with customers who have:

- Added experienced DevOps engineers who are comfortable building pipelines

- Reduced their Salesforce team size (reducing per-seat value)

- Come under pressure to consolidate vendor spend

A renewals function needs to quantify and communicate the "hidden cost of DIY" proactively — the engineering hours, brittleness, and lack of support that Gearset eliminates.

**3. Salesforce Team Headcount Volatility Hits Seat-Based Revenue**

If pricing is seat/user-based (as estimated), macro headwinds that cause customers to reduce Salesforce developer headcount directly compress renewal ARR — even when the customer is satisfied and retained. Given that Gearset's ICP includes companies running Salesforce as a core platform, economic downturns or Salesforce admin/developer layoffs (which happened materially across the ecosystem in 2023) create contraction risk that is hard to defend against regardless of relationship quality.

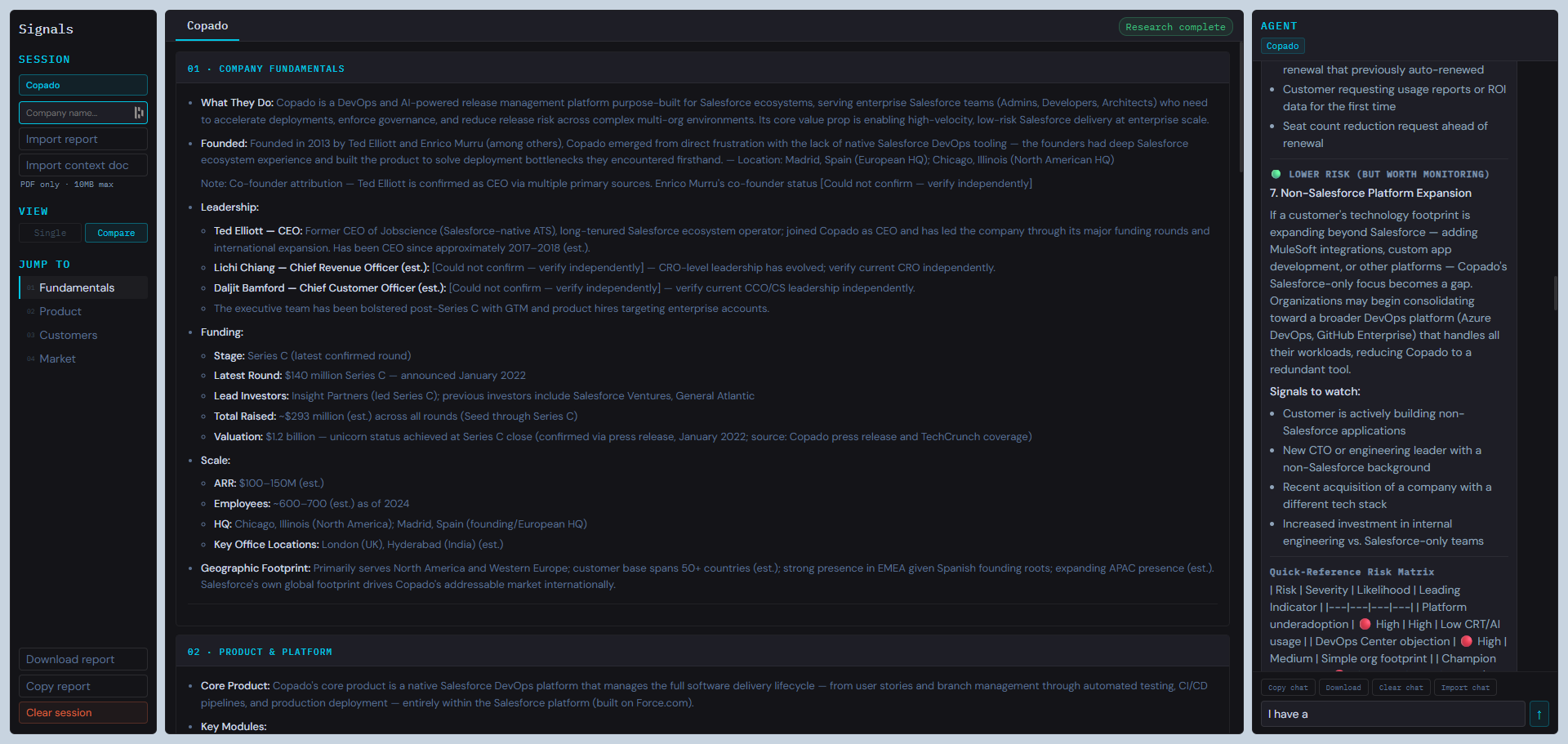

**4. Competitive Displacement Risk at the Enterprise Tier**

Copado has an aggressive enterprise sales motion with heavy Dreamforce presence and a broader feature set targeting large enterprise accounts. AutoRABIT competes on breadth (adding data backup/archiving that Gearset doesn't cover). At renewal, an enterprise customer receiving an active Copado or AutoRABIT proposal — particularly if they've grown in complexity and now have procurement leverage — creates a real displacement risk. A renewals leader needs to understand which accounts are actively being targeted by competitors and build executive sponsorship and multi-threaded relationships before renewal cycles open.

**5. Champion Turnover in Technical Buyer Roles**

Gearset's internal champion is typically a senior Salesforce Developer, Lead Architect, or Release Manager — not typically the CFO or CIO. These roles have above-average turnover in the Salesforce ecosystem (admin/developer career mobility is high). When the champion leaves, the institutional knowledge of why Gearset was chosen and the embedded switching cost rationale can evaporate quickly, especially if the new hire arrives with loyalty to a competitor they used previously. A robust renewals function would maintain multi-threaded relationships (including executive sponsor contacts) to survive champion turnover.

**6. Limited Visibility into SMB/Small Team Retention**

Smaller customers using Gearset primarily for basic metadata comparison — rather than the full CI/CD + compliance platform — have lower switching costs and lower expansion potential. These accounts may face pressure from Salesforce's own improving native tooling (Salesforce has been investing in DevOps Center, its native release management product) which, while not yet competitive with Gearset's depth, closes the gap for simpler use cases over time.

---

## The Salesforce DevOps Center Wildcard

Worth flagging specifically: **Salesforce launched DevOps Center** (GA in 2022–2023) as a free, native release management tool. While it currently lacks the depth of Gearset, it represents a "good enough" alternative for smaller or less technically sophisticated teams. Over time, continued Salesforce investment in native DevOps tooling is a structural headwind — particularly for Gearset's lower-complexity customers where the value differentiation is narrowest.

---

## What to Surface in Your Interview

Given this assessment, a sharp Head of Renewals candidate at Gearset should walk in ready to discuss:

1. **What is the current net revenue retention rate, and where does contraction come from — seat reduction, downgrades, or churn?** This surfaces whether the headwinds above are theoretical or already visible in the book.

2. **How is the renewals function structured relative to customer success and sales?** Given the PLG entry motion and enterprise expansion motion, there may be tension between these teams on account ownership.

3. **What is the protocol for accounts under competitive threat at renewal?** Specifically Copado displacement attempts.

4. **How does Gearset currently handle champion turnover risk?** Whether there's an executive business review (EBR) program or multi-threading discipline in place.

5. **What is Gearset's positioning response to Salesforce DevOps Center?** You'll hear this objection in renewal conversations with smaller accounts.

The renewals role at Gearset is a genuinely interesting one — the structural stickiness is real, but there are specific, well-defined risks that require active management rather than passive renewal processing.

**You:** Suggest several good questions I should consider asking during the interview process to gather useful information for how Gearset’s CS and renewal teams handle the Salesforce-Native security objection, DIY pipeline migration, and Salesforce team headcount volatility risks.

**Agent:** # Interview Questions: Probing Gearset's Renewal Risk Management

### Targeted Question Sets for Three Key Headwinds

---

A few framing notes before the questions: The best interview questions do double duty — they demonstrate your analytical preparation while surfacing information you actually need to evaluate the role. The questions below are structured to feel like informed curiosity, not an interrogation. Where relevant, I've noted what a strong vs. concerning answer looks like from your vantage point.

---

## Risk 1: Salesforce-Native Security Objection

**The core thing you need to know:** Does Gearset have a mature, documented response to this objection, or is it handled ad hoc by whoever is in the renewal conversation? Does the CS/renewals team own this or does it get escalated to sales engineers every time?

---

**Q1: "Have you seen the Salesforce-native security objection resurface at renewal for customers who were already live on Gearset — particularly after security reviews or leadership changes — and how does the team typically navigate that?"**

- *Why ask it:* Distinguishes whether this is a sales objection they've solved at the top of funnel versus a live renewal risk they're actively managing. The renewal context is specific — this isn't a prospect who hasn't bought yet, it's a customer whose security posture shifted post-implementation.

- *Strong answer:* They have specific examples, a documented response process, and ideally a security overview or compliance package that CS can deploy proactively. They know which customer segments are highest risk for this trigger.

- *Concerning answer:* They frame it purely as a sales objection with no acknowledgment that it can re-emerge at renewal. Or they say it "rarely comes up" without being able to explain why.

---

**Q2: "Does Gearset have a formal security and compliance resource package — trust documentation, penetration test results, SOC 2 reports — that the CS or renewals team can proactively share with customers ahead of renewal, particularly in financial services and insurance accounts?"**

- *Why ask it:* This is operational — you need to know what tools you'd actually have available to defend against this objection. A renewals leader without a strong security documentation package is fighting with one hand tied behind their back in regulated verticals.

- *Strong answer:* Yes, there's a formal trust/security package, it's maintained and updated, and CS has clear guidance on when to deploy it proactively versus reactively. Ideally there's a security review playbook.

- *Concerning answer:* This lives entirely with the sales engineering or legal team and CS has no independent access to it. Or it exists but hasn't been updated recently. Either signals a gap you'd need to build around.

---

**Q3: "How does the team currently handle accounts where a new CISO or IT security leader comes in and begins a vendor rationalization or security audit? Is there a proactive tracking mechanism for those types of stakeholder changes?"**

- *Why ask it:* Champion turnover in the security/IT leadership layer is the most dangerous trigger for the Salesforce-native objection — a new CISO arrives with Copado relationships or a preference for keeping everything on-platform. This question probes whether Gearset has built any early warning system for that risk.

- *Strong answer:* There's a defined process — CS monitors LinkedIn or uses a tool like Salesforce's own signals, EBRs include IT/security stakeholders, and there's a playbook for re-onboarding new security leaders to Gearset's trust posture.

- *Concerning answer:* The team finds out reactively when the renewal conversation gets difficult. No proactive stakeholder monitoring or executive relationship program exists above the champion level.

---

## Risk 2: DIY Pipeline Migration

**The core thing you need to know:** How well does Gearset quantify and communicate its value versus a DIY build? Is there a commercial or success framework that makes the "we'll build it ourselves" conversation concrete rather than abstract?

---

**Q4: "When a customer's engineering team grows in sophistication and starts questioning whether they could replicate Gearset's functionality with Salesforce CLI and GitHub Actions, how does the CS or renewals team typically reframe the value conversation? Is there a TCO or ROI model the team uses?"**

- *Why ask it:* The DIY objection is fundamentally a value conversation, not a product conversation. You need to know whether Gearset has invested in making the cost-of-DIY concrete — engineering hours, maintenance burden, support gaps — or whether CS is left making qualitative arguments that don't hold up against a CFO asking "why are we paying $50K for something our developers could build?"

- *Strong answer:* There's a documented TCO framework or ROI model CS can use, ideally with customer-validated data points. The team has a clear narrative around the hidden costs of maintaining DIY pipelines — brittleness, Salesforce release compatibility maintenance, lack of support escalation path.

- *Concerning answer:* The response is entirely product-feature focused ("but we do X, Y, Z") without a commercial/economic frame. Or the team acknowledges it's a common objection but hasn't built consistent tooling to address it.

---

**Q5: "Has Gearset experienced meaningful churn or downgrades specifically driven by customers migrating to self-built pipelines? And if so, what patterns did you see in those accounts — team size, tenure, industry — that might signal that risk earlier?"**

- *Why ask it:* This is a direct probe into whether the DIY risk is theoretical or already showing up in the churn data. If they've lost accounts to DIY, understanding the profile of those accounts tells you which segments of the renewal book to treat as highest risk. It also tests whether the team has done the analytical work to learn from that churn.

- *Strong answer:* They can speak to specific patterns — "it tends to be engineering-led companies with smaller Salesforce teams who brought in a DevOps-specialist hire" — and they've built those signals into their health scoring or at-risk identification framework.

- *Concerning answer:* "It doesn't really happen" without data to support that, or they can describe the churn but haven't done the pattern analysis to build a proactive response.

---

**Q6: "When Salesforce releases updates that break or require adjustments to customer pipeline configurations, how does Gearset communicate that to customers, and does the CS team use those moments proactively as value reinforcement — showing what Gearset handled that a DIY build would have required manual intervention to fix?"**

- *Why ask it:* Salesforce releases three major updates per year (Spring, Summer, Winter). Each release is an opportunity to demonstrate that Gearset's engineering team absorbed compatibility work that the customer's internal team would have had to do themselves. Whether CS is systematically capturing and communicating this is a good proxy for the maturity of the value communication program overall.

- *Strong answer:* There's a release communication cadence — release notes, proactive outreach, or in-app messaging — that explicitly calls out "here's what we handled for you." CS uses these moments in QBRs or renewal conversations as value proof points.

- *Concerning answer:* Release updates are handled reactively (support tickets when things break) with no proactive value communication program. A significant missed opportunity that you'd want to build.

---

## Risk 3: Salesforce Team Headcount Volatility

**The core thing you need to know:** How exposed is the ARR base to seat-count contraction, and does the renewals team have pricing strategies or contract structures that provide a buffer against headcount-driven compression?

---

**Q7: "How sensitive is the renewal book to Salesforce team headcount changes at customer accounts — if a customer reduces their Salesforce developer or admin headcount, what's the typical impact on their renewal ARR, and how does the team manage that commercially?"**

- *Why ask it:* This is the most direct question about the mechanics of headcount-driven contraction. You need to understand the actual pricing model exposure before you can assess the risk — and whether there are contract floors, minimum commitments, or org-based pricing elements that provide a buffer.

- *Strong answer:* They've modeled this exposure, know which accounts or segments are most sensitive, and have contract strategies (annual minimums, org-based tiers rather than pure per-seat) that limit downside. They may have intentionally shifted pricing structure to reduce headcount sensitivity.

- *Concerning answer:* Pure per-seat pricing with no floor, high concentration in tech/SaaS verticals that went through significant Salesforce team reductions in 2023, and no systematic monitoring of customer headcount signals.

---

**Q8: "Does Gearset track signals of Gearset Report

## Gearset — Full Report

═══════════════════════════════════════════════════════════════════

## 1. COMPANY FUNDAMENTALS

- **What They Do:** Gearset is a Salesforce DevOps platform that enables development and release management teams to deploy, test, and manage changes across Salesforce orgs with greater speed, reliability, and auditability. Its core value proposition is eliminating the complexity of Salesforce metadata deployments through CI/CD automation, version control integration, and compliance-ready pipelines — targeting Salesforce development teams at mid-market to enterprise companies.

- **Founded:** Founded in 2015 in Cambridge, UK, by Kevin Boyle and other co-founders with deep Salesforce ecosystem expertise. The founding team identified a critical pain point: Salesforce's native change set tooling was error-prone and lacked the version control and automation capabilities that modern software engineering teams expected, creating a clear founder-market fit around developer tooling for the Salesforce ecosystem.

- Co-founders: Kevin Boyle (CEO) confirmed via Gearset's own website and press materials; additional co-founder attribution: [Could not confirm — verify independently]

- **Leadership:**

- **Kevin Boyle — CEO & Co-founder:** Has led Gearset since inception; previously worked in software development and has been a consistent spokesperson in the Salesforce DevOps community, regularly appearing at Salesforce events (Dreamforce, TrailblazerDX) and DevOps-focused conferences.

- **Andy Mason — Head of Product (confirmed via LinkedIn and Gearset blog):** Leads product strategy and has been a visible voice in Gearset's product communications, publishing extensively on Salesforce DevOps best practices.

- **Additional C-suite depth:** [Could not confirm — verify independently] for CTO, CFO, and CRO titles/names from a primary source at time of research.

- **Funding:**

- **Stage:** Growth equity / Series B (est.)

- **Latest Round:** $55 million Series B raised in October 2022, led by Silversmith Capital Partners

- **Total Raised:** ~$55M+ (Silversmith was the lead; prior funding rounds were smaller seed/Series A — exact prior totals: [Could not confirm — verify independently])

- **Valuation:** [Could not confirm — verify independently]

- Source: Gearset official press release, October 2022; Crunchbase listing corroborates round size and lead investor.

- **Scale:**

- **ARR:** $30–60M (est.)

- **Employees:** ~300–400 (est.), based on LinkedIn headcount signals and company growth trajectory post-Series B

- **HQ:** Cambridge, United Kingdom

- **Key Office Locations:** Belfast, Northern Ireland (significant engineering hub); US presence (est.) in support/sales functions, specific US office location: [Could not confirm — verify independently]

- **Geographic Footprint:** Primarily serves customers in the United Kingdom, United States, Europe, and Australia (est.). The Salesforce ecosystem is global, and Gearset's SaaS delivery model supports customers across 50+ countries (est.). English-language primary; no confirmed localization into non-English markets at time of research.

---

## 2. PRODUCT & PLATFORM ANALYSIS

- **Core Product:** Gearset is a Salesforce DevOps platform that automates metadata deployments, integrates with version control systems (Git), and provides CI/CD pipeline orchestration specifically for Salesforce orgs — enabling teams to ship Salesforce changes faster and with fewer errors.

- **Key Modules:**

1. **Deployments & Metadata Comparison:** Core diff-and-deploy tooling that compares Salesforce orgs or branches and deploys selected metadata components — the foundational product capability.

2. **CI/CD Pipelines:** Automated pipelines that trigger deployments based on Git commits/pull requests, with built-in Salesforce-specific test execution and rollback capabilities.

3. **Data Deployments:** Allows teams to move Salesforce data (records) between orgs with referential integrity maintained — a distinct capability from metadata deployment.

4. **Monitoring & Compliance (Org Monitoring):** Continuous monitoring of Salesforce org configuration changes with alerting and audit trails, targeting regulated industries and compliance-conscious enterprises.